Beijing Auto Show 2026: Structural industry shifts on full display

From April 24 to May 3, the Beijing International Automotive Exhibition 2026 opened its doors. For ten days, Beijing became the global hotspot of the automotive industry. An exhibition area of 380,000 square meters across two combined exhibition centers, more than 1,000 exhibitors, almost 1,500 vehicles on display, and 1.28 million visitors made Auto China 2026 the auto show of superlatives.

The impressive scale of this exhibition, now the largest auto show in the world, illustrates the changes the automotive industry has undergone in recent years and decades in concentrated form. The center of innovation has shifted to China, particularly in NEVs, software, and development speed. Managers from established Western companies now come to China, marvel, and try to deal with the new reality in what is still their largest single market.

This broader shift manifests in many ways. In what follows, I want to describe three themes that currently stand out to me. None of them will be new to observers of the Chinese market, but all three were visible particularly clearly at Auto China 2026.

1. Flagship inflation

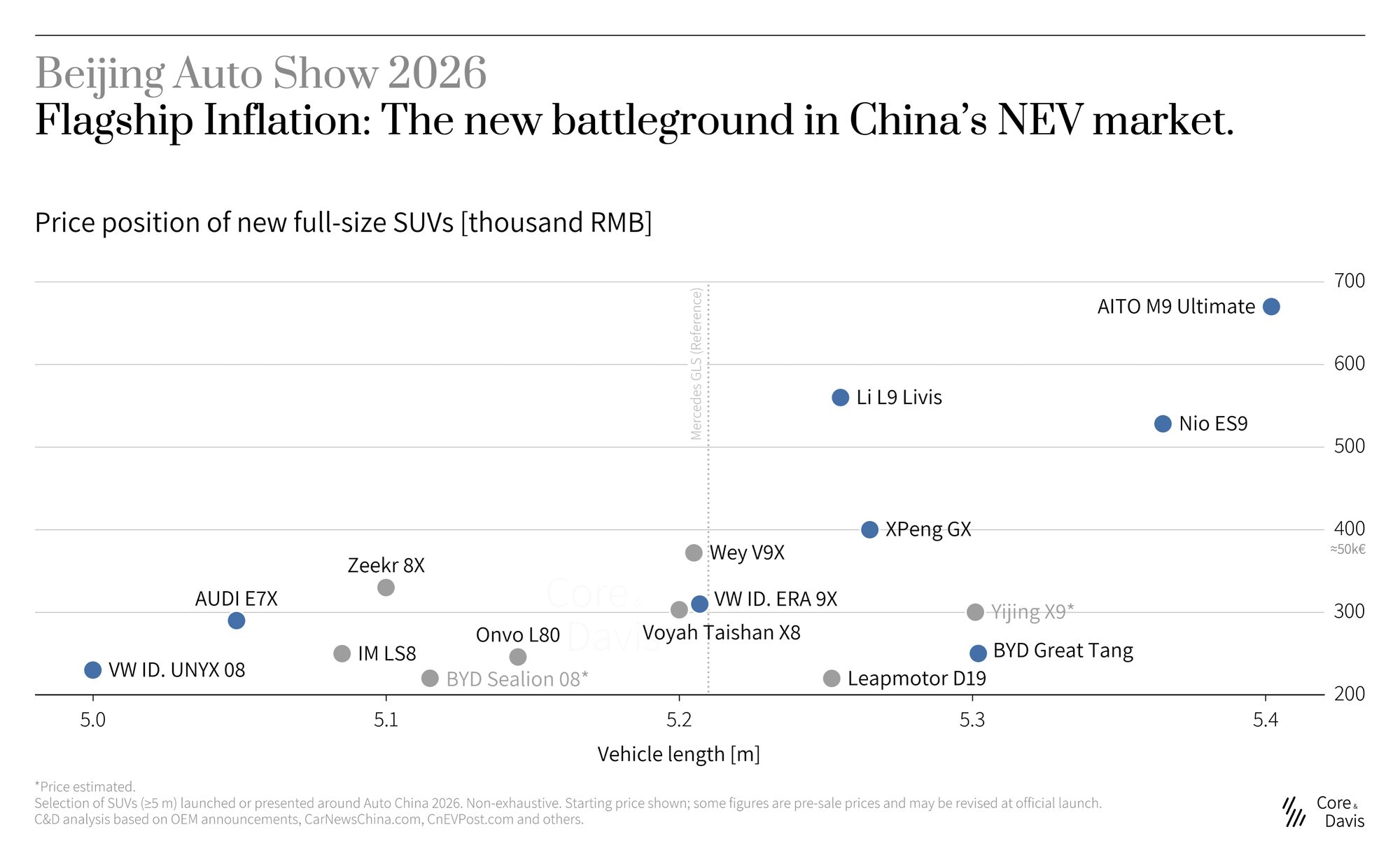

A phenomenon previously associated more with the US is now in full swing in China and was omnipresent at the auto show: large, comfortable SUVs, some well over five meters long, with more than enough room for the whole family. Nearly every Chinese brand seems to be launching one or even several of these "flagship models" right now. The cars offer luxury features that, until a few years ago, were known (if at all) only from the top models of German premium OEMs, along with tech features that make those very models look dated.

Huawei's brand AITO is extending its already GLS-sized M9 to over 5.4 meters to offer an even more luxurious variant. The price rises to the equivalent of over 80,000 €.

Li Auto, known primarily for its successful range-extender models, is taking a similar route: the L9 becomes the nearly 5.3-meter L9 Livis. Side note: it is being marketed with an impressive 2,560 TOPS of computing power and no fewer than four LiDAR sensors.

XPeng is presenting the GX, now the brand's largest and most expensive model, a direct competitor of the two vehicles just mentioned. BEV and REEV variants, up to 110 kWh of battery energy, and according to XPeng up to 3,000 TOPS of computing power, designed for L4 autonomous driving. Another push into the higher-margin premium segment.

The new flagship models from Li Auto and XPeng were both prominently displayed and attracted a lot of attention.

The trend is not limited to brands in the premium segment though:

BYD is launching the Great Tang, now the largest BYD brand model, and doing so with success: according to BYD, more than 100,000 pre-orders came in within less than two weeks of pre-sales opening.

Leapmotor, already active in Europe as well, is expanding its portfolio with the full-size SUV D19. In China, rices start at the equivalent of under 30,000 €.

VW is the first German OEM to follow suit, launching the ID. ERA 9X, a full-size SUV with a range extender for just under 40,000 €. The 9X is the largest vehicle in the brand's lineup, was developed in China, and (as of today) is offered only there.

The chart shows further examples, with the most notable ones highlighted in blue. The background to this "flagship inflation"? The segment promises higher margins, which are essential for survival in this fiercely competitive market, meets strong customer demand right now, and was until recently rather sparsely populated. Now, however, Chinese manufacturers have the technology and the confidence to push into this territory as well.

2. In China, for China

The advance of local OEMs into higher segments is becoming a problem particularly for German automakers, which, like other foreign OEMs, are continuously losing market share in China. They are now increasingly trying to reverse the trend with products more closely tailored to the Chinese market, often developed locally and with local partners. Comparatively young Chinese companies are meant to help the long-established OEMs become competitive again. This remarkable new reality is visible at Auto China in the most literal sense: in the spotlight of the booth of Momenta, a company founded only in 2016 and specializing in autonomous driving, is a Mercedes GLC.

A Mercedes-Benz GLC in the center of the Momenta booth and BMW promoting "In China. For China. With China." Source (right picture): BMW Group.

The GLC is no exception. The result of OEMs' localization efforts is on display this year in the form of numerous product launches. From my perspective, three categories can be distinguished:

Long wheelbase

The familiar approach. German OEMs in particular have been extending their models for the Chinese market for many years to give rear-seat passengers more space. By now, even Tesla offers an extended Model Y exclusively in China.

Local tech

Going well beyond just mechanical extension is the integration of local technology, which is taking place particularly in the areas of autonomous driving and software. Momenta plays a major role at this year's show: the company's ADAS solutions can be found, for example, in the Mercedes GLC (as in the previously launched CLA), several BMW models, the VW ID. ERA 9X, and the Nissan NX8. Equally omnipresent: Huawei, for instance in the Audi A6L (ADAS) or the Toyota bZ7 (e-drive, OS). More on Huawei later.

China-only products

The clearest admission by foreign OEMs that they cannot compete in China with global products. Vehicles exclusively for the local market, developed in China, often with local partners. The VW Group in particular is rolling out a wave of new products in this category in Beijing, all packed with innovations from China:

- AUDI E7X (SAIC-Audi): The sub-brand newly created in 2024 without the four-ring Audi logo is now presenting the SUV E7X, its second model after the AUDI E5. With a base price of 290,000 RMB, it is positioned roughly on par with the somewhat smaller Audi Q6L e-tron, despite a larger battery. The technical innovations? Made in China.

- VW ID. ERA 9X (SAIC-VW): The China-developed VW flagship, as mentioned above. Under the metal, there is presumably some kinship with the IM LS9 (a SAIC brand). VW's first REEV, developed and brought to market in record time by legacy OEM standards.

- VW ID. UNYX 08 (VW Anhui): A large SUV, five meters long, fully electric. According to Volkswagen, developed in just 24 months. The first market launch of a model emerging from the partnership with XPeng. Entry price: 230,000 RMB (about 29,000 €).

- VW ID. UNYX 09 (VW Anhui): Another flagship model, this time as a sedan. World premiere at the Beijing Auto Show, market launch expected later this year.

- VW ID. AURA T6 (FAW-VW): A mid-size SUV, the first model of the ID. AURA sub-brand. Also a world premiere.

AUDI E7X and VW ID. ERA 9X. Source: Volkswagen AG.

As these examples show, the VW Group's brand and product portfolio in China is extensive and complex. I may publish a separate analysis on this, hopefully then with initial sales figures for the newly introduced models.

Other examples:

- Toyota bZ7: Full-size electric sedan (5.13 m long), 600–710 km of electric range (CLTC), just over 200 kW of drive power. Electric drivetrain and infotainment OS from Huawei, ADAS solution from Momenta, built by the joint venture GAC Toyota. Starting at 180,000 RMB (around 22,500 €).

- Nissan NX8: Mid-size SUV with BEV and REEV powertrains, 800-volt architecture, up to 460 kW charging power, built by Nissan's joint venture in China, Dongfeng Nissan. Pricing starts at 160,000 RMB, roughly 20,000 €.

3. Tech dominance and Huawei's role in it

Many of the vehicles on display at Auto China 2026, especially the flagship models from Chinese manufacturers mentioned above, are packed with cutting-edge technology made in China — not only in ADAS and software. High-performance computing platforms with chips that are in some cases developed in-house, as at XPeng and Li Auto; extensive LiDAR and sensor stacks; the most advanced batteries from market leaders CATL or BYD with charging times in the single-digit minute range; steer-by-wire and active suspensions. China is now the lead market for new technologies in these areas. The pace of innovation is enormous, and initially expensive technology quickly reaches the mass market, as the examples of LiDAR and steer-by-wire show.

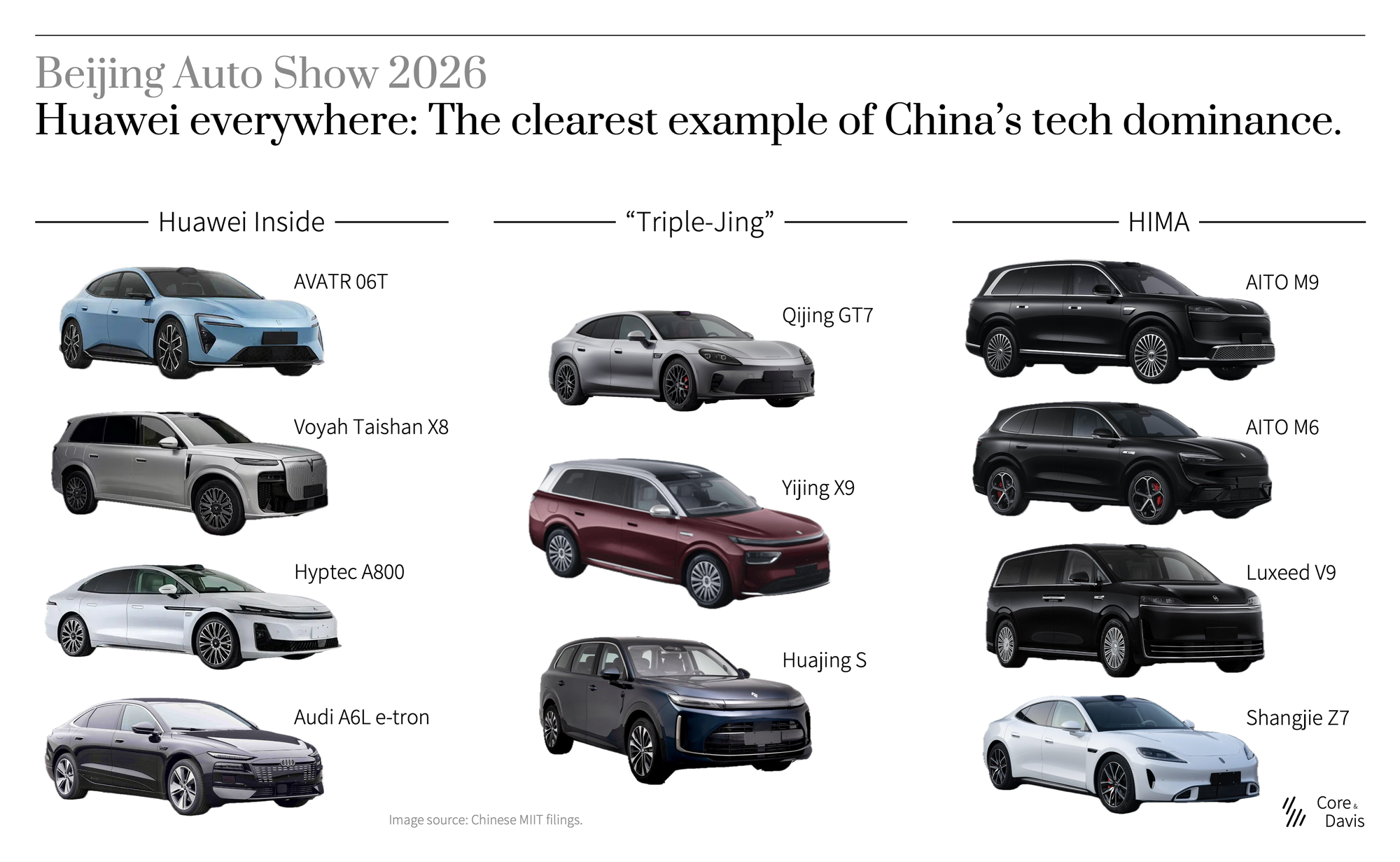

One company has assumed a position that makes it structurally important for both Chinese OEMs (matching 1.) and foreign ones (matching 2.): Huawei. Huawei is neither a classical supplier nor a classical OEM in the automotive industry. The company pursues a multi-track approach and is currently omnipresent at the auto show as well as in the automotive landscape in China:

Component supply

Conventional supplier business model. Under brand names such as Qiankun and Harmony, Huawei delivers various components and systems, from LiDAR and cameras to infotainment software to drivetrain and chassis components.

"Huawei Inside" (HI / HI Plus)

The not always clearly distinguishable extension of the classical component-supply model. Huawei delivers a complete hardware and/or software stack, primarily in ADAS ("Qiankun Smart Driving") and cockpit ("HarmonySpace"). Control over the end product remains with the purchasing OEM; depending on the arrangement, Huawei is more or less heavily involved. Show debuts that fall into this category: the 06T, a wagon from AVATR; the Voyah Taishan X8; and the Hyptec A800. Notable: Audi can be classified as the first non-Chinese brand in this category. The Audi A6L e-tron presented at Auto China runs, like other vehicles from the brand before it, on Huawei's Qiankun ADAS technology.

"Triple-Jing"

Joint vehicle development with another OEM, with Huawei additionally contributing complete system solutions analogous to HI. The newest of the four engagement models, with the three brands Qijing (Aistaland, with GAC), Yijing (Epicland, with Dongfeng), and Huajing (with SAIC-GM-Wuling). The first vehicle of each of the three brands was presented at this auto show: the electric shooting brake Qijing GT7 and, matching the flagship inflation narrative, the over-five-meter SUVs Yijing X9 and Huajing S.

HIMA

Huawei's well-known Harmony Intelligent Mobility Alliance with the five brands AITO (with Seres), Luxeed (with Chery), Stelato (with BAIC), Maextro (with JAC), and Shangjie (with SAIC). Huawei controls product strategy, development, marketing, and sales channels; the cooperation partner produces the vehicles. In 2025, the HIMA alliance delivered nearly 600,000 vehicles, around 70 % of them under the AITO brand. At the auto show in Beijing, alongside numerous updates to existing models, several new alliance vehicles were presented: the Ultimate variant of the AITO M9 mentioned above, the mid-size SUV AITO M6, the van Luxeed V9, and the Shangjie Z7/Z7T (visually reminiscent of the Porsche Taycan) as a sedan and shooting brake.

In total, more than a dozen brands are showing new or updated vehicles at this year's Auto China in which Huawei is more or less heavily involved, visible proof of the dominance Huawei has built up in the Chinese automotive industry in just a few years. This brings us full circle: the Huawei example illustrates once again the shift of the automotive innovation center to China described at the beginning of this article.